According to Solarbuzz’s latest report on Asia Pacific's major terminal markets, the Asia-Pacific PV market will grow rapidly, and the proportion of total global demand is expected to grow from 11% in 2010 to about 1/4 in 2015. The top five markets in the region - China, Japan, India, Australia and South Korea - will have a total market demand of 3.3 GW in 2011, while China and Japan will be separated by one or two.

According to Solarbuzz’s latest report on Asia Pacific's major terminal markets, the Asia-Pacific PV market will grow rapidly, and the proportion of total global demand is expected to grow from 11% in 2010 to about 1/4 in 2015. The top five markets in the region - China, Japan, India, Australia and South Korea - will have a total market demand of 3.3 GW in 2011, while China and Japan will be separated by one or two. The major Asian and Pacific regional markets are now undergoing major policy changes. Mainland China, India, and Australia have all started to build a grid-connected market, and Japan and South Korea are facing policy changes that will once again stimulate their domestic demand for the next two years. As the output of Chinese mainland manufacturers reaches 50% of the world, their domestic demand is also encouraged by the national and provincial government policies. In 2011, the scale of China's PV market could expand by up to 174% over 2010.

“The growth of the Asia-Pacific market is expected to be high, especially in mainland China and India with several GW projects to be installed. However, the biggest challenge comes from ensuring the financial support of these projects in an ever-changing policy and regulatory environment.†Craig Stevens, Solarbuzz general manager said. "If these policies succeed in helping the Asian-Pacific market grow, it will be beneficial to reduce the impact of the subsidies cut in the European market."

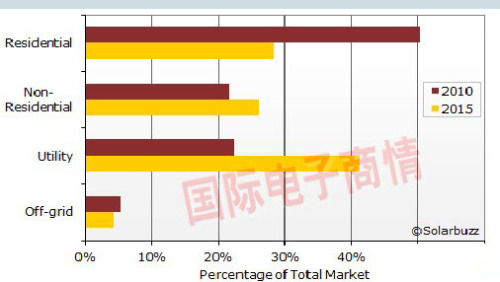

In the category of customers, utility demand will lead the growth of demand in the Asian solar market, replacing residential installations as the largest customer category in the future.

Japan's solar power growth encouraged by new policies With the implementation of the purchase price subsidy policy, the Japanese solar power market is expected to have at least 1.29 GW of new installations in 2011, equivalent to an annual growth rate of 35%, and the current low level of European solar power. The market is in stark contrast. Although the installation of non-residential types is not yet the most installed type, this year's growth rate is more than double the growth of residential installations. In 2010, Japan was the fourth-largest solar energy market in the world. Its annual installation capacity has also tripled from the past to 960MW, thanks to the government's resumption of full-fledged residential subsidies and incentives to purchase electricity prices. The Fukushima nuclear disaster also caused Japan’s domestic solar cell makers to vociferously raise the renewable energy bill. At the same time, the number of components imported from abroad also has an annual growth rate of 138%, which accounted for 13% of the total shipments of components in Japan last year.

China's solar power market is ready to break through the GW scale In China, large-scale and utility-scale projects are stepping up with incentives, and grid-connected installations are forecast to double in 2011. In 2010, 85% of the Chinese market demand came from projects with a scale of more than 1MW. In the near future, the grid-connected electricity price in Qinghai Province will further expand the proportion of ground-based utility projects in 2011. Projects such as the Golden Sun Project and solar roof power generation continue to advance and urge developers to complete the installation as soon as possible. The purchase price policies of Jiangsu Province and Shandong Province also make a significant contribution to the overall demand. With the improvement of the policy environment of the central and local governments and the close to 10GW of projects to be installed, the Chinese PV market will continue its strong growth all the way to 2015.

India's grid-connected market with strong growth grid-connected ground-based projects is expected to lead India’s total installed growth and is expected to grow at least twice in 2011. The National Solar Mission and state policies such as Gujarat, Rajasthan, and Maharasgtra lead the growth of demand. The demand of these three states together account for 70% of India's 2011 solar market. In order to reach the target of newly installed capacity exceeding 22 GW by 2022, the national solar task has approved a 300 MW grid-connected power generation installation capacity between 2011 and 2012, and will allocate another 300 MW installation capacity in the second half of 2011. Although problems such as high capital investment, low remuneration, and regulatory obstacles have emerged in the first round of projects, it is likely that future projects will be restructured to encourage higher success rates. As of June 2011, the grid-connected project is expected to have installed 1.5GW by 2013.

South Korea's policy-oriented renewable energy quota system Despite the negative growth caused by the end of the government's repurchase electricity price plan in 2011, the long-term growth potential of South Korea’s solar power generation remains stable through the implementation of the renewable energy quota system. The new renewable energy quota system is expected to bring in 1.2GW of new installations in the next five years, but such growth has been slow compared to the past. After reducing the incentives for the repurchase electricity price and the renewable energy quota system, the large-scale ground-mounted projects significantly slowed down in 2010, while the solar power generation projects of the building type grew strongly. As the South Korean government intends to encourage small-scale and building-type solar power generation, this trend will continue in the coming years.

Australia's solar energy market is not affected by the volatile policies and continues to hold the long-term Australian government’s latest energy policy to impose carbon taxation. It will transition to the “limit-trade†system in 2015. The new policy followed several dramatic policy changes, including the acceleration of the rate of decline of the main subsidy policy, solar credit, and the reversal of several state-level repurchase tariffs. Despite the Australian government's attempt to dominate the solar installation demand, the market still grew by 431% in 2010. As the installation cost of solar power systems decreases with the decline of global module prices, the increase of certified installers, and the expected increase in retail electricity prices, the economic efficiency of photovoltaic systems has greatly improved. New South Wales accounts for 44% of the national market, but the suspension of the solar energy bonus plan in April has now caused the market to collapse. For Australia, fragmented and inconsistent policies remain the biggest stumbling block for the long-term sustainable development of the solar energy industry.

Chongqing Taishan Cable Co., Ltd. , http://www.cqbareconductor.com