Lei Feng Network (search "Lei Feng Network" public concern) by: Author of this article Chen Da (Snowball: Chen Damei stock investment), Master of Business Administration (MBA), investment consultants.

Needless to say, the Netflix model is the future.

A long time ago, a company called Blockbuster dominated the rental disc industry for many years. A man named Reed Hastings rented a disc there, and he was angered by the overdue return of a "big" overdue fee (about $40). Then he went to work hard and found that the business model of the gym is very beautiful. No matter how much you go or how little, the membership fee can not be paid less.

Unfortunately, Hastings is a software engineer who is about to change the world at every turn. The idea has to be done. What's worse is that he was already very rich. As a result, he founded Netflix in addition to his anger. He also did a rent-disc business with no overdue fees and membership. Thirteen years later Netflix put Blockbuster in bankruptcy protection.

This story tells us two reasons:

1. Customer service must be done well. Don't kill the wool. If you don't, you'll force the sheep to be a tiger.

2, engineers can not afford it.

Of course, Blockbuster cannot be said to have lost its life. In fact, she represents the past and lost to the future. Obviously, Netflix is ​​the future. But Blockbuster isn't suddenly defeated. Specifically, she was subjected to the long and brutal torture of the double evolution of the Netflix business model.

business modelNetflix Business Model 1.0

Netflix at this stage only made a brave evolution on the Blockbuster model.

Blockbuster model is very simple: you come to my shop, I rent your disc, expired repayment, not withholding money. At first glance, this is not a rented video rental bookstore at the door of the house after the 1980s. Where the earlier Blockbuster was more in place than other competitors, it used data to analyze the demographic characteristics of the surrounding inhabitants and to determine the type of Tibetan discs. This business model has an image named Landlord, which means that I have assets and I'll rent it for you for the time being.

By the way, almost all of the business models that follow traceability can be attributed to the following four images: Creator, Distributor, Landlord, and Broker.

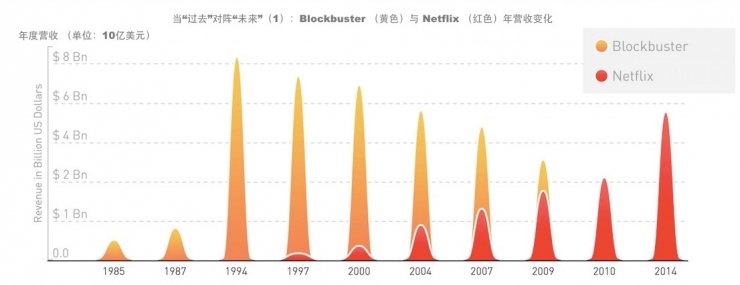

Blockbuster has eliminated a large number of local “front-end rented disc stores†through franchising and leading-edge data analysis. Ironically, Netflix’s elimination of her later use is also one step ahead of big data analytics. At the peak of 2004, Blockbuster, which represents the “pastâ€, has a total of more than 9,000 stores and nearly 60,000 employees. So at the beginning of the founding, Netflix did seem to have something to do with Don Quixote pumping in front of the big windmill. At least, some of the most far-sighted analysts on Wall Street had a rather polite and euphemistic comment on it: A worthless piece of crap. Now she is worth 36 billion U.S. dollars!

At the beginning of the 1.0 evolution, Netflix only made two changes to the Blockbuster pattern:

1, light assets, no storefront, online operations.

2, mail to home. Users order discs online, Netflix mails them to customers overnight, and customers read Netflix by mail.

Compared to Blockbuster, the direct comparative advantage of this operation is:

1, O2O, can not go out, provincial leg.

2. How to choose, Blockbuster how to adjust the Tibetan plate according to the population data, but also can not stand the line of others online selection.

What Netflix does at this point is pondering a question: How can a user experience better than renting a disc from Blockbuster? Many people think that Netflix uses the Flat rate (fixed rate) monthly membership system and does not charge for overdue fees. Actually, Netflix is ​​also a step-by-step experiment. The initial charge is for each half of the disc. Compared to Blockbuster's average of five knives each, it is already very obvious that the four-and-a-half spread has made Netflix far to the right on the demand curve.

In September 1999, Netflix finally launched a non-membership system with no expiry date, no overdue fees, and no postage, with a monthly subscription fee of 19.95 knives and a maximum of four discs at a time. Just cancelling the overdue fee can be a big hole in Blockbuster, because Blockbuster customers are really miserable to this cost, have fallen. Someone asked if Blockbuster wouldn’t have any kind of overdue fees? The fact is that overdue fees accounted for 16% of Blockbuster's total revenue. Listed companies have to explain to shareholders that the thigh meat cannot be easily cut. Of course, this piece of meat was still cut, Blockbuster also tried to build the online rent dish platform Total Access, but in the end could not stop the giant incumbent in situ explosion.

A map can depict the future of Netflix Battle on behalf of the past Blockbuster Tiangou food and moon general scene:

You say that Netflix has enough confidence in extinguishing the old ally. In fact, it is a step-by-step step forward and step by step. There was such a sad reminder in the 2002 prospectus: “From the beginning to the present, we have accumulated a loss of days, and we even have an equity deficit of $90 million (balance sheet liabilities are greater than assets). We need to The earth improves our operating margin (Operating Margin) to achieve profitability. We may never be profitable."

Netflix Business Model 2.0

After a counterattack with 1.0 to become a new ally, Netflix began to ponder another issue no matter what: How can the user experience better than renting a disc from Netflix? We arrived in 2006, the first year of Netflix Streaming. By that time, Netflix had had 4.2 million subscriptions and the basic service fee had dropped to 17.99. You said that the idea of ​​streaming media was very sexy and novel at that time. Actually, it was impossible to talk about it. In 1995, some people tried to engage in streaming media business. However, the problem is that technology can't keep up with inspiration. The next time it takes time to grow into cabbage, etc. Old pickles. This also shows that the prerequisite for the new concept to make money must be technology in place, not Vice Versa (reverse), think about the current AI (artificial intelligence) and VR (virtual reality).

In 2006, the broadband penetration rate of American households rose by 40% from 2005 to 84 million; there is another, perhaps more important, data change: Compared to 2005, the family’s total annual income is between 40,000 and 50,000 knives. In the family, broadband penetration has surged by 70%. what does this mean? This shows that the youngest and most leisurely people most likely to not watch TV and use Netflix services are suddenly networked. According to a commercial law that I personally believe in, “they have to get the world under the wireâ€, this should be the flow of development. The best time of the media, it seems that the east wind has arrived. Another major event in 2005 also made it possible for the "streaming media" experiment to still achieve its first big victory: YouTube turned out.

Whether it is renting a dish or streaming media, the core value of the Netflix business is not changed: VoD (Video on Demand) content is on-demand, and it is different from the traditional live streaming (LIve Streaming) .

At this point, the streaming media is clearly able to win over the rent dish, so we have seen Netflix start to attack itself once. Netflix's streaming media has several advantages in terms of visibility:

1. Cheaper, the monthly fee drops below $10, and goes further on the demand curve.

2, cross-platform, TV, PC, Wii, PlayStation, XBox, you name it, personalized settings to go with the account, you can change the platform from the previous point of memory can be broadcast.

3, the user's personalized settings.

4, no advertising or "promotion" or whatever.

5, Self-made content (Netflix Originals), content self-sufficiency in innovation, in-depth content layout.

In 2005 before the streaming media, Netflix had 4.2 million subscribers; in 2016, Netflix had 83.2 million subscriptions in 2016, a good one-year round of 100 million.

Moat survey (comparative advantage analysis)I don't have much to say about the obvious advantages of Netflix, such as the global market and the Economies of Scales. But you have to say that it is not a moat in an absolute sense. This is an issue for benevolent people.

I think the scale advantage is not really a true moat in this industry, because according to the harsh definition of Pharaonic, this river refers to the company's ability to last long to stop the competition and maintain long-term profitability. The scale advantage may still be a moat in the retail industry. However, in the streaming media VoD industry, because there were no copyright barriers in the early days, predecessors who had the advantage of having a priori and having scale advantages couldn't say no if they couldn't (even in the United States, they didn't have to talk about it), but Blockbuster took a few short years. People's sadness precedent. The industry with rapid technological innovation, the scale advantage is not a thing in front of the chaos that the influx of innovative competitors, said that if you get rid of your results, you will kill you too much .

Talk about what I think Netflix really moats.

Content Portfolio

There is no doubt that Netflix's content reserves are very impressive. If you want to watch all the contents of Netflix, it will take almost four years to brush up and play without food or sleep. But one of the more confusing facts is that compared to 2014, the current total content of Netflix has shrunk by 32%. In January 2014, Netflix provided 6,484 movies and 1,609 episodes to U.S. users; however, by March 2016, the number had shrunk to 4,335 movies and 1,197 episodes.

Netflix explained that they excluded a lot of non-exclusive content and tried to keep the team pure . For example, The Hunger Game series is also available on Amazon, so Netflix has not been renewed after the copyright expires. Instead, Hulu shouted.

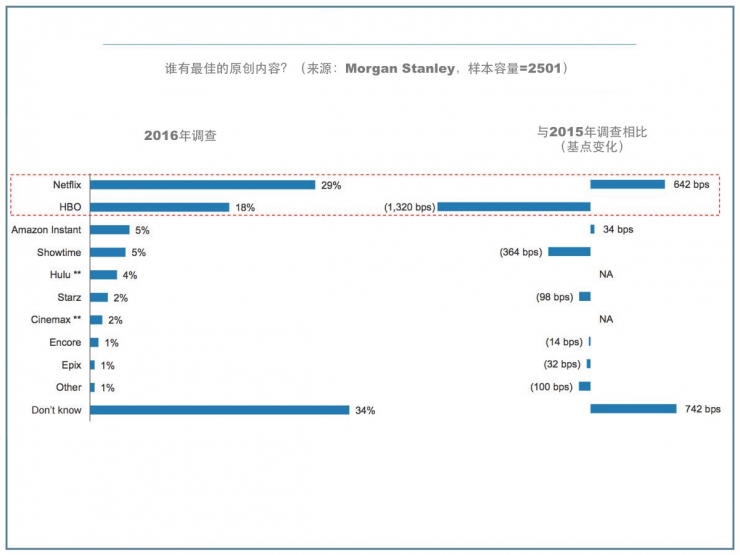

So we see that Netflix's current focus is not on volume but on quality, especially on the exclusive nature of content. This is of course a chiseling idea for the city, so that an addictive user can't make a difference, because many contents have no branches. The current questionnaire survey conducted by major organizations also shows that Netflix's content is a bit to protect the city. For example, Morgan Stanley's representative sample survey of people over the age of 18 (sample size = 2501) showed that 29% of the respondents indicated that the content is not Netflix, while 18% believe that it is HBO (Time Warner's pay-TV network). And these two are far ahead of other competitors. The specific data can refer to the following figure.

It can be seen that Netflix is ​​very aggressive in terms of content in recent years. Of course, it is like investing in aphrodisiacs. In 2012, Netflix's investment in content is approximately US$2 billion, and in 2016, it is expected to invest US$6 billion (1.2 billion yuan in original content). For a company that expects to generate revenue of approximately 8 billion in 2016... Flowers open to be discounted?

Netflix's original content is also very competitive in professional awards. In the just-released 2016 Emmy nomination list, Netflix received 54 Primetime Emmy nominations, second only to FX (Fox's FX TV) and HBO; and harvested 33 daytime hours Nominations (Daytime Emmy nominations), first for all networks. Taking into account the history of Netflix's home-made dramas for only a short period of three years, it has made a great success. Netflix's proud productions include the House of Cards, the Orange is the New Black, the Making a Murderer, the Narcos, etc. In addition to seeing half of the women’s prison abandoning the show, the other departments are all pushing and pushing.

Technology and Big Data Applications

Amazon seems to be in the retail industry, but in fact she is a technology company; Tesla seems to be in the car industry, but in fact she is a technology company; Netflix looks in the entertainment industry, but in fact she is a technology company. From the beginning, singled out Blockbuster, Netflix is ​​playing the concept of an O2O, can not be separated from the open information technology. Even more so today, Netflix is ​​notoriously driving the industry's top-paying lantern-hunting IT engineer. The company also runs the Netflix Tech Blog on the official website to discuss cutting-edge technical issues.

Netflix technology applications essentially answer two questions:

1. How to improve user viewing experience?

2. How to cast users on content?

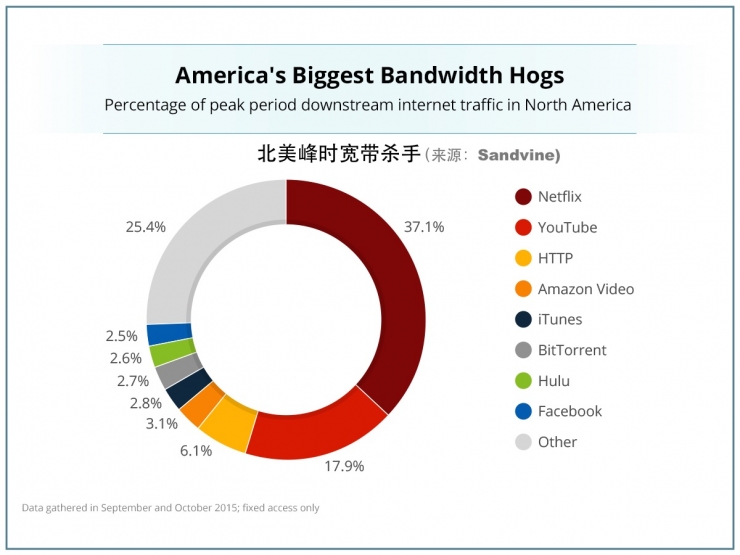

Netflix’s answer to the first question is very sincere to me. According to the above data, Netflix occupies one third of the bandwidth of North America's entire Internet during peak hours, and the throughput is quite alarming. Regardless of whether the user's bandwidth is fat or thin, the most basic experience needs are two things: to be HD and to be smooth. But higher picture quality and less bandwidth are often a beautiful paradox. This requires Netflix to use streaming bandwidth saving technology.

For example, most streaming media companies will determine the quality of the transmission based on the user's bandwidth. For example, on a good weekend night you go to bed early and want to watch an action movie. As a result, the buddies who sleep on your upper floor are playing LOL. So you watch your HD video become standard definition and then become smooth video and finally become not smooth video. Of course, this technology Netflix also used, each video has a number of different quality video files to support a 235kbps bandwidth can transmit 320x240 screen, 5800kbps bandwidth can transmit 1080p video. But there is a problem, in order to adapt to the bandwidth limitations, the same size and use the same Encoding technology, compression of a "World of Warcraft" is certainly more ambiguous than the compression of a "SpongeBob SquarePants", the image quality loss even more severe.

So Netflix's algorithm team spent four years re-coding these things, instead of doing a uniform rough one-size-fits-all approach, but according to the characteristics of each resource, the Title by title basis, fine processing, each film will Get different algorithms. This technology can save the user 20% of the bandwidth, while improving the quality of the picture, to solve the beautiful fallacies. How Netflix engineers are willing to do fine? They think that even if they are the same episode, each episode is different, and each episode should have its own Encoding.

Regarding the second question, Netflix's answer is to analyze the big data that has been talked about for many years, and use this as a starting point to carry out user recommendations and create original content, and use big data to shoot "big numbers." This estimate is very familiar to everyone, but I would like to ask why we all know that Netflix is ​​a big data company? The major TV stations also have their own spectator data. HBO and other subscribers have more than 50 million subscribers, but why do you know that Netflix is ​​playing big data and playing with it? Why is this?

Because Netflix wants you to know. This is a gimmick for PR propaganda. For example, what kind of competition is to design a big prize to attract talents from all walks of life to provide various algorithms, such as using big data to analyze and customize “card house†and achieve unprecedented success. As a junior, Netflix is ​​actually walking on thin ice. Before that, she said that she first took Blockbuster to the next level, and now she has to start clapping with the industry's oldest TV makers. All of them are big men with large waists and thick legs. How can the pressure on the PR come up and grab the customer?

When the Internet is overwhelmingly advocating Netflix to use big data to analyze user viewing habits, you will psychologically accept all the Netflix recommend to you: Well, I see you recommend it anyway, I have been analyzed by you through the see. However, if you look closely you will find: Netflix's original content is always at the front. Well, maybe Netflix has seen it. I just like to watch the Netflix original series.

I don’t believe I can make a hot show just because of big data. Netflix and Hemlock Grove (Hydrangea Grove) after “Board of Fortunesâ€. Amazon also depends on big data and called Alpha House. Episodes, but it is clear that these "big dramas" have no fire. To tell the truth, before the launch of a drama, the heart of the fire could not be counted. The taste of the audience did not have the same level of standard as a monkey. Whoever guessed. So the advantages of Netflix big data analysis above are not a moat in the end. I am skeptical that I dare not draw a conclusion and who will dare to go. However, I believe that the big money can make a hot drama: Topstar, Yanming, top production team, and PR publicity, how come the big thing; and this is not exactly what Netflix did when playing the card house?

The castle was picked up and the moat dug out. Next, we started to attack the city.

financial dataLook at the financial performance first (the currency unit is the US dollar).

In 2016, Q1 and Q2 earnings were 27.66 million and 40.76 million. In Q3 and Q4 in 2015, they were 29.43 million and 43.18 million. TTM (most recent 12 months) was 0.29 per share, and TTM price-to-earnings ratio was 300X; 2016Q3 and Q4 earnings per share were estimated to be 0.06. And 0.07, 2016 earnings per share forecast of 0.28, Forward ing price-earnings ratio is still 300X, of course, three hundred times the price-earnings ratio is not enough to scare us, we have seen met with even if there is no price-earnings ratio, and have long been accustomed to numbness. TTM revenue of 7.6 billion, TTM sales rate of 5X, which is still definitive, the rapid growth of revenue has always been Netflix's strengths.

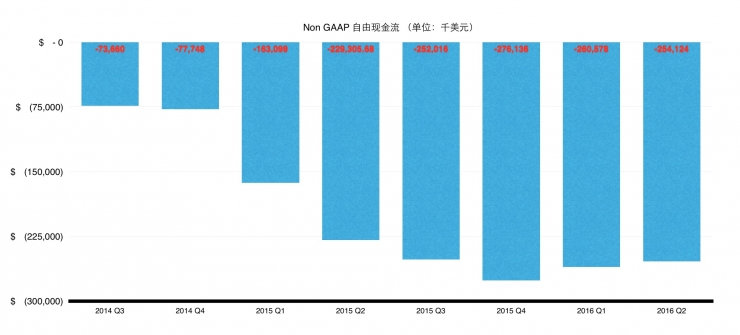

But the focus is cash flow. Netflix users are growing rapidly. Everyone thinks that this product must be a cash cow, but Netflix is ​​actually a golden cow . In fact, Netflix's cash flow from operating activities has been negative since 2014, and it has become increasingly belligerent. In Q2 2016, it reached -2.26 billion. TTM has been operating cash for the past year. Nearly 900 million flows, and free cash flow is -1.04 billion. For a long time, it was like a fat man who had been chopped by 80 knives at the crime scene. However, it is clear that the net profit is a large positive number, but the cash flow is so unbearable?

Those who know a little bit about the operating cash flow or the free cash flow calculation method know that both positive net profit and negative cash flow are generally due to accrual Basis (Accrual Basis). Time to confirm, rather than the timing of cash entry, generates non-cash income or cash expenses are not expensed resulting in an increase in non-cash assets.

In Netflix's cash flow statement, there is a big reduction in the process of using the indirect method to generate cash flow from profit: Additions to streaming content assets, which is the annual quarterly cash The chief culprit of the outflow. It may be that some people will ask, can you speak people? In the big white sense, the reason for the miserable cash flow is because Netflix has always been relentless in the first line of filming. You have to spend money to make a big cash out, but the income statement doesn't count the expense, but instead is included in the content assets after being fixed, and then amortized every year; so the cash flow and net profit will appear time difference in the financial statements. .

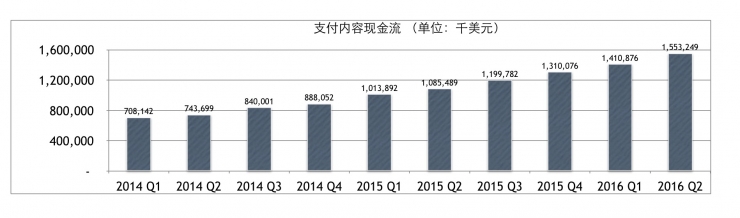

As mentioned earlier, one of Netflix’s most important moats is content, but maintaining the moat requires a capital. From Netflix's cash flow statement, we can figure out how much Netflix spends each year or quarterly on content:

Compare Additions to streaming content assets and Change in streaming content liabilities, and watch how much real money is thrown into this moat every quarter:

In the last 12 months, it totaled 5.47 billion, and Netflix officials expect it to be 6 billion in 2016. From a quarterly perspective, cash spent on content has doubled in just ten quarters. Of course, some people may say that the number of users does not increase in a double-fold manner. The cost of content should naturally rise. After all, there is no wolf where there is no tram. With regard to Netflix's investment in content, we can spread the content to each user.

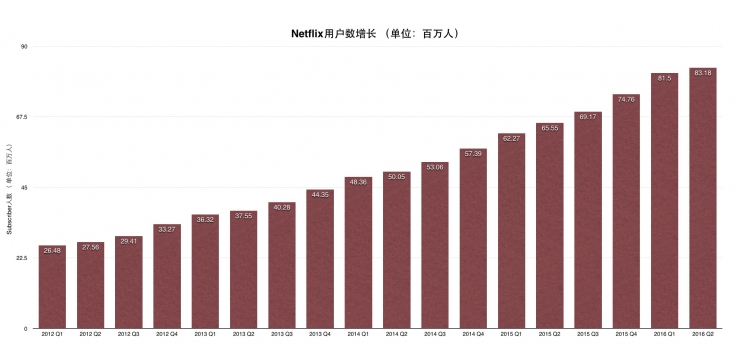

The following is the quarterly number of users.

Dividing the previous figure before the previous one can give:

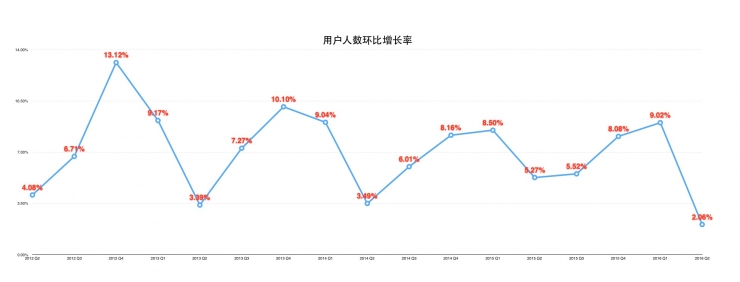

We can see that the spending on content paid for each individual is actually showing a rising trend, and the ideal scale effect is currently not realized. The reason is that Netflix's user growth has shown a trend of decline. Netflix spends more and more money on the content has been more and more difficult to pull the number of users, the marginal effect diminishes the iron rule. This is not a good thing for a so-called "growth stock" whose share price is clearly dominated by user growth.

Another person would ask: Since this golden donation is so strong, where does Kim come from? Simple, borrow money. I find that when we talk about Netflix, we don’t talk about debts. Is it because we are growing stocks and you don’t care about the source of financing? In Q2 2014, the long-term debt was 890 million, in Q2 2015 it was 2.37 billion, in Q2 2016 it was 2.37 billion, and TTM interest expense was 140 million, which measures the interest coverage ratio of the company's interest repayment ability (the higher the interest rate ratio, the ability to pay interest The stronger is 1.89X (EBIT/interest expense), which is close to the vigilant 1.5X alert line. Of course, the highest proportion of Netflix liabilities is not long-term debt, but about the current and long-term liabilities of content, which is close to 6 billion, resulting in Debt to equity ratio = total debt/owner equity = 3.8, whether it is Tech industry or entertainment Industry, the industry average is certainly less than 1.

Of course, we can still tolerate "certain" "special" companies with high leverage because at least they still have dreams. However, in the "Investor FAQ" section on the company's official website, the sharp question about "How are you going to invest in content?" The company's magnanimous answer is "We plan to use high-interest debt financing." So in the future, Netflix’s debt will only build higher, but people are not failing to tell you; if this happens later, you still have to carry your own back.

Industry and competitionLet us leave behind the financial unhappiness, put aside the unpleasant figures and charts first, talk about quality issues, and talk about Netflix's industry. I said before that I think Netflix's broadest moat is technology and the other is content, and it's clear that the company is developing around these two priorities; but if I'm a Netflix shareholder, I would like her to simply be a technology company. And don't go into the army to prepare for the brilliant filmmaking industry.

why?

Because I hate the film industry. At least, the filmmaking industry is a grievance business for the company's shareholders, because the star's remuneration is basically high enough to be shameless, and the production company has no pricing power. I remember Mr. Qiu Guolu’s book “The simplest thing in investingâ€. He said that the business model of pure movie shooting has internal injuries. Everyone watches movies. They are all rushing and they are just ah. As the name leads, no one will go for a production company. You can't hear people say, "I watched movies on the Huayi Brothers," or "I'm the brain of a Changchun movie studio." Therefore, so many movie companies in the United States must eventually become vassals of a certain media group, because only the single business model of filming can't live at all; but Disney lives well because Mickey Mouse and Donald Duck never ask for it. rise salary.

All industries that have a high cost of human resources are not a good industry. It's like I have a little bit of a stake in Manchester United football club for a long time, but am I investing? Absolutely not, it's purely a brainwashing thing to satisfy my feelings. From the point of view of the rate of return, the club can be said to be the worst investment. You can see that Rooney’s salary is 260,000 pounds per week. These are plainly from the pockets of shareholders. Yahoo CEO Marissa Mayer paid $36 million in 2015 and was repeatedly criticized for his high salary. However, Rooney’s compensation for one person in 2015 was already 17 million. The problem is that Manchester United also has more than a dozen small Rooney’s and weekly salary. The 100,000 pounds are common, which is equivalent to other large companies raising more than a dozen top salary CEOs at the same time.

But there is no way ah football is a special undertaking. This dozens of uncles are the core assets of the club and they must be provided at all costs. Another example is that Manchester United wants to buy Juventus's Bogba, which will cost 120 million euros. The deal has turned out. Fans, of course, are happy to see that it is not Lao Tzu's money. But as a Manchester United shareholder, it should be extremely embarrassing.

So I think the production industry is an unlovable industry; but Netflix is ​​on the ups and downs, but it is an inevitable choice, because in fact she has no other choice.

We all know that for investors, the best industry is a monopoly industry, and monopoly means pricing, which means that producer surplus (Producer Surplus) is not necessarily a good thing for social welfare, but it is certainly short-term for shareholders. It is a good thing.

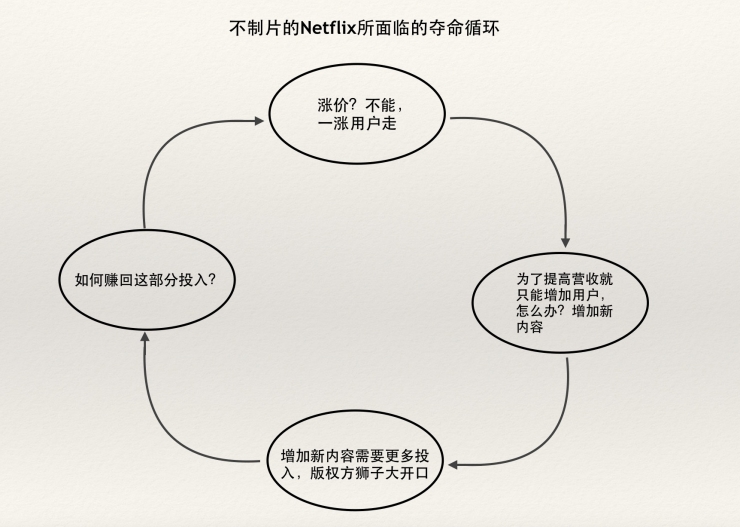

Firms have pricing rights, whether it is external product service pricing or internal human resource pricing or pricing for upstream suppliers, but did Netflix ever have? No, it has not been a price hike since she has largely eliminated Blockbuster with price advantage. Netflix even gave back to the promise of a lifetime of users, guaranteeing $7.99/month to remain unchanged. This is called the Grandfather Clause (meaning to maintain the validity of old contracts for certain users). On the other hand, there is no pricing power for upstream content provider Netflix. Content prices are rising year after year. If you don't embark on the road to production, Netflix will fall into the following fatal cycle:

Once Netflix was trapped in this painful closed loop, they could only increase content and constantly try to increase the number of users, but never to make money.

To break this closed loop can only rely on price increases, to increase prices but there is no loss of users, can only develop user stickiness in the content, so homemade content becomes almost the only export. So it's not hard to understand that Netflix has to go home for self-produced content. The key to Netflix's success, which comes from Chief Content Officer (CCO) Ted Sarandos, is to see Is "Netflix becoming HBO faster, or HBO becoming Netflix faster."

But can you grab the pricing right this way?

Not to mention that the filmmaking industry mentioned before may not be a good industry for shareholders. The model of streaming media+original content is being used by rushed competitors because the threshold of this industry is actually not high, and the powerful Tech company basically It means to engage even more. So we see that Netflix's opponents line up to get out of a mighty team:

1. Amazon launched Prime Video Streaming and Disney.

2. The media giants of the 21st Century Fox and Comcast jointly launched Hulu and Hulu Plus.

3. HBO launches HBO Now and HBO Go.

4. Dish launched Sling TV.

5. Google has YouTube Red and plans to launch YouTube Unplugged for TV Streaming next year.

6, Facebook is also recruiting to find media companies to find stars to find online red.

7. Wal-Mart acquired Vudu with the media.

8, even on the side of the sand playing Apple is also eyeing, it is not a day or two to come to personally gossip Streaming rumors, and before HBO directly hooked together to engage in HBO Now.

It's true that Netflix is ​​still the best in the industry; but it is embarrassing that its butt is glued to the boss of other industries whose strength is raging.

Netflix Competitors' Matrix

The competition and meddling of the streaming media industry will only become more and more unrestrained, and the surplus of the industry's producers will only become increasingly barren . Netflix is ​​painstakingly trying to break the painful closed loop, but breaking it will really usher in the light of time.

Netflix is ​​undoubtedly a great company, but it is a lifestyle creator. For example, there is a saying in the United States called Netflix and Chill, which means "Look at Netflix's contract about Pao." (Sisters don't want to hear each other say Let's Netflix and Chill are naive to think that it's only time to take a look at the film and relax and then gladly go to the appointment.) Netflix culture has penetrated the market and bone marrow. But just don't know if Netflix's shareholders can achieve Chill in the midst of the upcoming ice and fire. In light of the current financial situation and the status quo of the industry, I sincerely do nothing for them.

Although Netflix is ​​more than fierce, it's not my favorite fish.

The author of this article does not hold the aforementioned stock positions. The article was authorised by the author to release Lei Feng Net.

158.75 mono perc half cells

Solar Cells Module,Half Cut Cells,Solar Cut Cells,Solar Panel

Zhejiang G&P New Energy Technology Co.,Ltd , https://www.solarpanelgp.com